The Great-Power Financial Model

Julkaistu: 21.06.2011

The Great-Power Financial Model

A smouldering conflict between the East and the West, a token of modern times, continues to penetrate into every sphere of social life. And the economy is no exception: Sharia regulated banks are offered as an alternative to banking principles formed in medieval Europe. Sharia (Islamic law) is the code of conduct for a Muslim, with its precepts set forth in the Qur'an. The main factor preconditioning the specifics of Islamic economy and Islamic banking (or participant banking) is prohibition of specific interest for money loans.

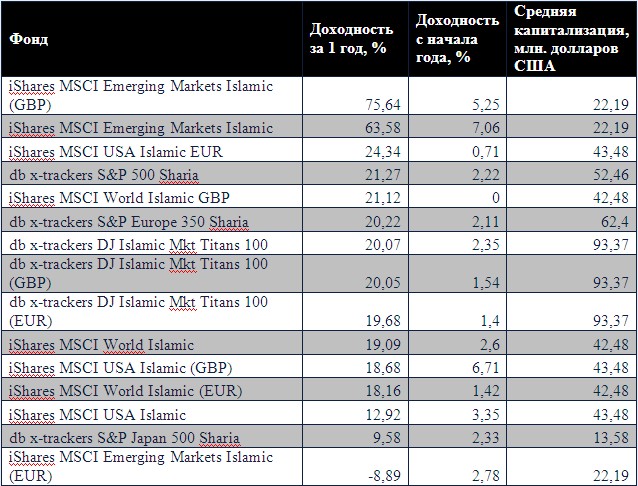

So, what is going on with the “barbarian” East? According to HSBS banking grand, modern Islamic banking industry worth about $6 billion is serviced by nearly 500 financial institutes spread inside and outside the Muslim world. Certainly, so far this represents approximately 0.5% of total world volumes. Still, Islamic banks manage about $1 trillion assets and they are growing at a rate of 10–15% per year. It is worth noting that over the last years their growth rate hovered around the same 15% as though the global financial crisis was no concern of theirs.

A historical reference: commercial Islamic banks as we know them appeared in the middle of 70s, when Dubai Islamic Bank was set up in 1975. The evolution of Islamic banking was facilitated by two factors: predictable dramatic rise of revenues from supplies of black gold and the Islamic revolution in Iran. However, even Islamic bankers admit that in many aspects the Islamic financial model: a) is far from being perfect; b) does not strictly conform to Islamic canons; c) does not offer real advantages to its customers. Then, what could be the secret of its growing halal popularity?

In all sincerity, over the last 20 years Islamic banking failed to improve financial situation in the countries where it was most popular: at the Middle East and in Southeast Asia (Iran, Katar, Malaysia, Emirates, Pakistan). Islamic banks did not become a viable alternative to secular banks; that is just a myth evoked by the Qur'an. The essence of the two systems is almost the same; they differ only in description adapted for ideas of the Muslim world. And the interest rate in such banks may be even higher.

To our thinking, the main difference between the secular bank and the Islamic one is as follows: when coming to a religious bank, the person is sure that he is doing everything right. In countries where average income is not enough for satisfying personal needs, a reasonable man is constantly choosing, but every variant he prefers brings infringement of certain interests with it.

Robert Kiyosaki, the one who is an investor and a writer, called this phenomenon by an impartial term “the rat race”. In general, the religion becomes a guideline for the bank’s client. Even if he misses his financial wellbeing in a terrestrial life, then at least he is offered peace of mind for his financial choice guaranteed by God.

Having switched to global discourse, let us turn to a factor of multiculturalism. At present, Islamic banks are functioning in Germany and in France, in the USA and in Japan, covering more than 70 countries of the world. Recently, Europe has declared the end of the immortal multiculturalism. While its Islamic population continues to grow, the region may face a rapid growth of banking institutions. But these will be Islamic banks, or rather “Islamic windows”—branches of traditional banks offering banking services that comply with the Muslim laws. So, the Muslims are to get their own loan institutions… but the underlying banking principles will remain secular, after all. And the new institutions will be beneficial for European economy attracting additional assets of those who would rather trust them to higher powers.

The official statistic says there are about 20 million Muslims living in Russia. Though it is impossible to tell the exact number, it is certainly higher than in France or India.

Debates and roundtables about the Islamic capital entering Russian banking market started only in 2009. Kazan hosts international summits of Islamic business and finance. The latest major event that took place during the 4th international peacemaking forum “Islam—the religion of peace and creation”, Grozny, May 2011, was a roundtable on prospects of Islamic banking in Russia. Following the event, a proposition was made to create a working group which would prepare legislative and regulatory base with further submitting it to the government of Russia for implementation of Islamic finance and insurance projects in the Chechen Republic.

At present, the progress of Islamic banking in Russia is impeded by loan institutions, which are unsure whether the demand is high enough. Moreover, there are certain legislative barriers. Thorough changes in the Civil Code are a must. Banking laws and instructions are to be updated, too. With regard to the above mentioned initiatives, one may suggest future progress in this sphere. As for the demand, so far experts consider it to be minimal but with high growth potential as the Muslims of Russia become more and more active in financial and economic issues. Taking into consideration a stable demand for halal food, the market can well transform into a considerable one. According to a research of the Russian Centre for Islamic Economics and Finances, in future the amount of population savings potentially attracted to Russian economy on Islamic principles could be as high as 60 billion roubles. The Association of Regional Banks of Russia is sure that aims and objectives of Islamic financial services development in Russia should be covered in the Russian Banking Sector Development Strategy up to 2015 and in the Concept of Creating an International Financial Centre.

Large finance institutions have been keeping an eye on a promising segment for some time already. In 2009, VTB-Capital announced plans to release Islamic bonds (the so called “sukuks”). The bank was ready for an emission worth $200 to 300 million. But the project was postponed first till 2010, and then till 2011… The partner of VTB-Capital for sukuks is Liquidity Management House, a branch of Kuwait Finance House. Sberbank has also discussed a possible issue of sukuks some time ago. A few pro-islamic monetary consumer cooperatives (Amanat, Kazan) and trust partnerships (Umart-Finance, Kazan) are functioning already, while BKS-Halal unit fund remains a unique structure for Russia.

After all, the Islamic financial model turns out to be promising, irrespective of its strict compliance to the Islam. First of all, its crisis resistance is higher to due to prohibited mortgage bonds and certain secondary securities. Secondly, it is demanded. And finally, it may appear economically viable.

We have already mentioned a multiculturalism aspect of Islamic financial model in Europe. And what about Russia? The necessity to develop this segment is, in the majority of cases, associated with the Chechen Republic and Tatarstan. These regions are usually regarded as subjected to separatism though it is hardly possible to imagine the circumstances under which they could lay a claim for sovereignty.

But an initiative of a religious character, and where! at the Caucasus!.. In their speeches, our politicians may mention the region as very promising, but such things come into direct conflict with the current trend for unification or, in plain words, for strengthening the central power.

The proposition to combine European and Sharia financial models in Russia will be sure to cause a myriad of useless political discussions. Meanwhile, objective processes of economic development will move in the opposite direction. The future (though not so close) is to bring the financial market a number of Islamic financial products.

Still, the above mentioned discussions will give birth to an idea of some domestic, Orthodox variant as opposed to Islamic banking. The process has already begun with a roundtable “Orthodox Banking and Financial Tools in Russia” hosted by the Association of Orthodox Businessman in January 2011.

The current legislation for religious institutions sees no obstacles for church establishments to participate in the capital of commercial banks. In fact, banks partnering with the church have been functioning in Russia since 90s (Peresvet bank, Blagovest bank with its license now deprived, and the notorious International Bank of the Redeemer Cathedral). The boom of the “Orthodox” banking has already passed. But in case of campaign for Islamic financial products one may expect its revival at a stepped-up pace and with strongly pronounced Orthodox shade. We have already clarified that the client of a “religious” bank gets his peace of mind along with the assurance (at least, assurance in his future life). And, sad as it may seem, for Russian reality this is quite a pressing point.

In contrast to the Islam, the Orthodox Church does not put any theological demands for financial operations. It means that God-pleasing principles of a new, Orthodox financial model are to be invented yet. And the resources spent for it will be surely not less than for updating the legislation for further introduction of Islamic financial tools.

Foreign media names total absence of governmental support to be the main obstacle for integrating certain elements of Islamic financial model in Russia. The invisible hand of the market has crashed once more over a stable sovereign democracy. Here, Sharia finances are rooting in a local no-analog model. We shall call it a great-power one.

Send message